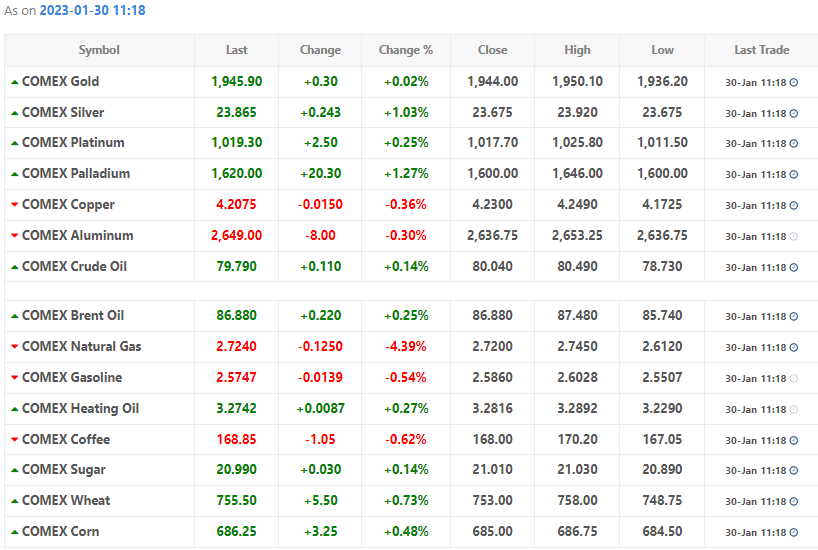

Oil prices rose about 2% on Thursday on expectations that global demand will strengthen as top oil importer China reopens its economy and on positive U.S. economic data.

Brent futures rose $1.35, or 1.6%, to settle at $87.47 a barrel, while U.S. West Texas Intermediate (WTI) crude rose 86 cents, or 1.1%, to settle at $81.01.

The U.S. economy grew faster than expected in the fourth quarter, but a measure of domestic demand rose at its slowest pace in 2-1/2 years, reflecting higher borrowing costs.

“Crude prices got an unexpected boost from a U.S. economy that doesn’t want to break,” said Edward Moya, senior market analyst at data and analytics firm OANDA.

U.S. crude inventories edged up by 533,000 barrels to 448.5 million barrels in the week ending Jan. 20, the Energy Information Administration (EIA) said.

That was short of forecasts for a 1 million barrel rise, though the EIA says crude stocks are at their highest since June 2021.

China has been easing stringent COVID-19 restrictions this month, with Beijing reopening borders for the first time in three years.

“China’s reopening is supporting demand prospects,” said UBS analyst Giovanni Staunovo.

“Also, market participants are closely tracking the upcoming OPEC+ JMMC (Joint Ministerial Monitoring Committee) meeting and the EU (European Union) embargo on refined products,” Staunovo said.

The Organization of the Petroleum Exporting Countries (OPEC) and their allies, including Russia, are collectively known as OPEC+.

The OPEC+ ministerial panel meeting on Feb. 1 is likely to endorse the oil producer group’s current output levels, OPEC+ sources said.

Global economic growth is forecast to barely move above 2% this year, a Reuters poll of economists showed, suggesting a further downgrade is possible. That was at odds with widespread optimism in markets since the beginning of the year.