Oil futures recouped some losses on Wednesday, recovering from a 2% slide in the previous session, supported by supply concerns stemming from last week’s OPEC+ cut to its production target, though a stronger dollar weighed on sentiment.

Brent crude futures were up 37 cents, or 0.4%, at $94.66 a barrel after touching a session low of $93.33.

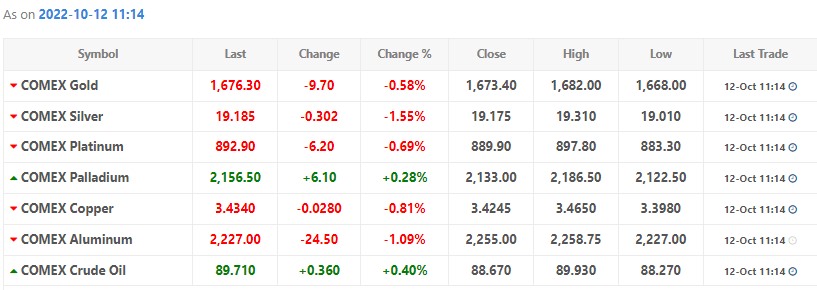

U.S. West Texas Intermediate crude was up 18 cents, or 0.2%, at $89.53 after a session low of $88.27.

“There are two dominant forces in the oil market at the moment; the economic outlook being the primary downside risk and OPEC+ the upside,” said OANDA analyst Craig Erlam.

“The latter reasserted itself last week with the 2 million barrel per day cut … but growth fears are still dominating in the markets, which may stop the price from taking off.”

Last week, the Organization of the Petroleum Exporting Countries (OPEC) and allies including Russia, together known as OPEC+, decided to cut their output target by 2 million barrels per day (bpd).

“Although OPEC+’s 2 million bpd headline oil output cut from the August quotas looks large on paper, the effective cut would be smaller,” Citi Research said in a note, adding that it expects the final cut to be less than 900,000 bpd, partly owing to poor compliance from Iraq.

Also on the supply side, Russia’s state-owned pipeline monopoly Transneft on Wednesday said it had received notice from Polish operator PERN about a leak on the Druzhba oil pipeline, Interfax reported.

Meanwhile, the U.S. dollar hit a 24-year high against the yen on Wednesday on concerns about inflation and the pace of increases to U.S. interest rates.

A stronger dollar makes dollar-denominated commodities more expensive for holders of other currencies and tends to weigh on oil and other risk assets.

Also on the downside, the International Monetary Fund on Tuesday cut its global growth forecast for 2023 and warned of increasing risk of a global recession.

The U.S. consumer prices report is due on Thursday.