Oil prices rose on Tuesday after China posted its second-weakest annual economic growth in nearly half a century, though its recent shift in Covid-19 policy underpinned hopes of a recovery in fuel demand this year.

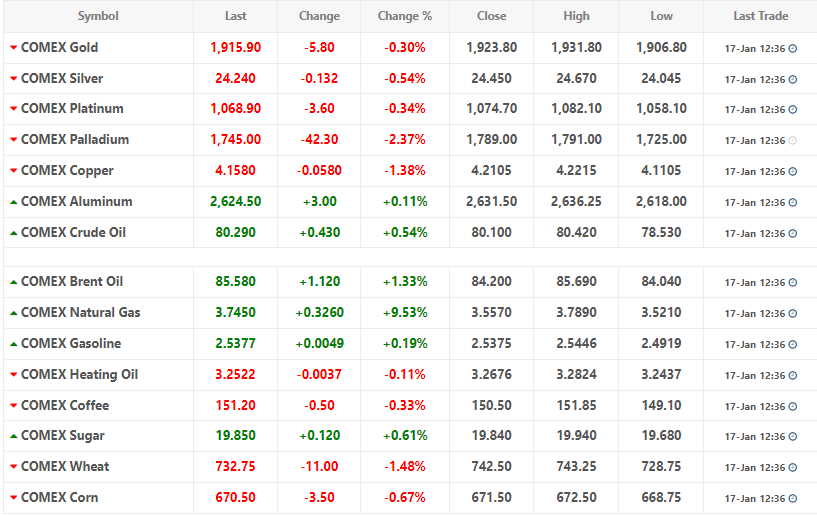

Brent crude futures rose $1.18 cents, or 1.4%, to $85.65 a barrel. U.S. West Texas Intermediate (WTI) crude wadded 49 cents, or 0.6%, at $80.35.

There was no settlement on Monday because of the U.S. public holiday for Martin Luther King Day.

China’s gross domestic product expanded 3% in 2022, missing the official target of “around 5.5%” and marking the second-worst performance since 1976, hit by Covid curbs and a property market slump.

The economic data still beat analysts’ earlier forecasts after Beijing’s rolling back of its zero-Covid policy in December bolstered consumption.

Data released on Tuesday showed China’s oil refinery output in 2022 had fallen 3.4% from a year earlier for its first annual decline since 2001, though daily December oil throughput rose to the second-highest level of 2022.

“The country’s crude oil imports were up 4% in December and a considerable demand boost for transportation fuel … is anticipated when the Lunar New Year begins on Sunday,” said PVM analyst Tamas Varga.

He added that reports from the Organization of the Petroleum Exporting Countries (OPEC) on Tuesday and the International Energy Agency (IEA) on Wednesday will shed more light on the strength of oil demand while recession fears loom.

In a survey released at the annual World Economic Forum in Davos, two thirds of private and public sector economists polled expected a global recession this year, with about 18% considering it “extremely likely”.

A survey of chief executives’ views by PwC was the gloomiest since the poll was launched a decade ago.

A slight strengthening of the dollar from seven-month lows also pressured oil prices, making dollar-priced oil more expensive for buyers holding other currencies.