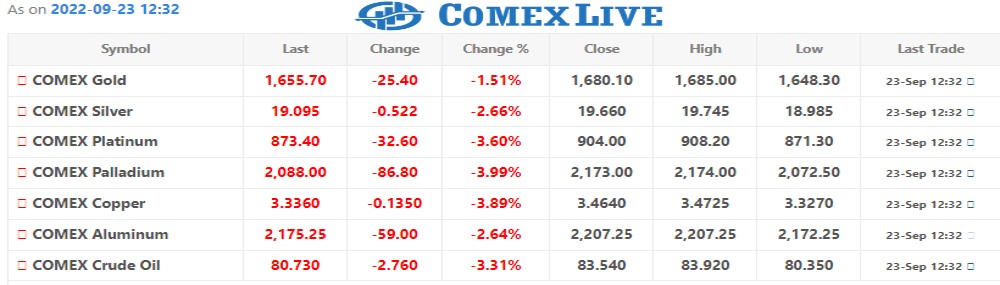

Oil prices fell on Friday as demand fears were stoked by rising interest rates and a stronger dollar, though losses were capped by Moscow’s mobilization campaign in its war with Ukraine and apparent deadlock in talks on reviving the Iran nuclear deal.

Brent crude futures fell $2.81, or 3.11%, to $87.65 a barrel by 1051 GMT. U.S. West Texas Intermediate (WTI) crude futures were also down, retreating by $2.93, or 3.51%, to $80.56.

Front-month Brent and WTI contracts were down 4.03% and 5.37% respectively over the past week.

Global equities hit a two-year low on Friday while the dollar index reached its highest level in two decades, putting downward pressure on oil.

“Recession fears, further rate hikes and the consequent dollar strength trumps geopolitical tension,” said Tamas Varga, oil analyst at PVM Oil Associates.

“The upside in oil will be limited while the dollar is strong, albeit the weekend’s staged referendum in the eastern part of Ukraine could further increase tension between Russia and the West, especially if Ukrainian allies provide additional help for Ukraine to reclaim these territories.”

Russia launched referendums on Friday aimed at annexing four occupied regions of Ukraine, which Kyiv called an illegal sham that it said included threats to residents if they do not vote.

After the U.S. Federal Reserve raised interest rates by a hefty 75 basis points on Wednesday, central banks around the world followed suit with hikes of their own, raising the risk of economic slowdowns.

A downturn in business activity across the euro zone deepened in September, a survey showed, suggesting that a recession is looming as consumers rein in spending to contend with a cost of living crisis.

In Britain, meanwhile, the pound fell to a 37-year low and government bonds crashed after the new finance minister announced historic tax cuts and huge increases to borrowing.