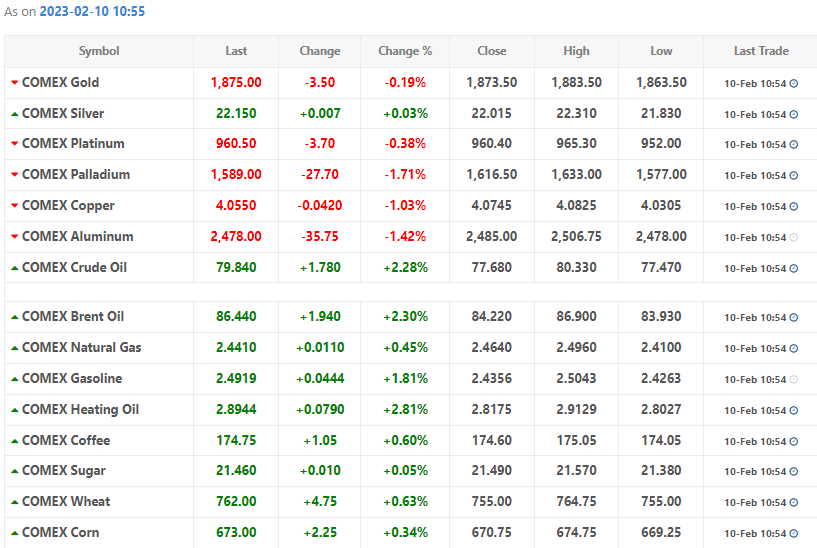

Oil prices fell in early trade on Friday but were headed for a weekly gain with the market continuing to seesaw between fears of a recession hitting the United States and hopes for strong fuel demand recovery in China, the world’s top oil importer.

Brent crude futures fell 28 cents, or 0.3%, to $84.22 a barrel by 0117 GMT, while U.S. West Texas Intermediate (WTI) crude futures fell 35 cents, or 0.5%, to $77.71.

The downturn was partly due to a report on Thursday showing the number of Americans claiming unemployment benefits increased more than expected last week, which reignited recession fears.

“Sentiment overnight seemed to be tilted towards the downside after the jobless data in the U.S. — however I expect the China demand recovery will be more material to the price outlook into (the second half of) 2023,” said Baden Moore, National Australia Bank’s head of commodity research.

The latest U.S. oil inventory data this week also raised fears about a slowdown in the world’s biggest economy, with crude stocks having climbed to their highest since June 2021.

Nevertheless Brent and WTI have jumped more than 5% so far this week, reversing most of last week’s losses as concerns about further sharp interest rate hikes by the U.S. Federal Reserve have eased.

The lower rate hike expectations drove the dollar down, which in turn supported oil prices. A weaker greenback makes oil cheaper for holders of other currencies and often sparks buying.

The market has also been buoyed by Saudi Arabia’s move to increase its official crude sales prices to Asia, seen as signaling a demand recovery in China.

Analysts said U.S. inflation data on Feb. 14 will be key to risk sentiment and the dollar’s direction.

“As inflation declines across Europe and the U.S., risks remain elevated that central banks will need to still deliver more tightening than what markets are pricing in,” OANDA analyst Edward Moya said in a note.