Oil prices rose for a fourth session on Thursday, with Brent at a three-week high, after OPEC+ agreed to further tighten global crude supply with a deal to slash production by about 2 million barrel per day, the largest reduction since 2020.

Brent crude futures for December settlement rose 22 cents, or 0.2%, to $93.59 per barrel by 0234 GMT after settling 1.7% higher in the previous session.

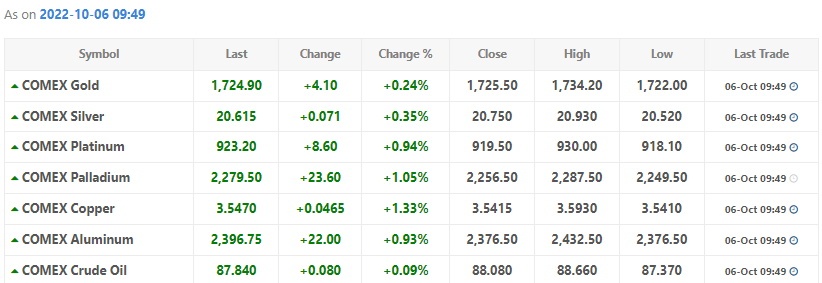

U.S. West Texas Intermediate crude futures for November delivery gained 22 cents, or 0.3%, to $87.98 per barrel, building on a 1.4% rise on Tuesday.

The agreement between the Organization of Petroleum Exporting Countries and allies including Russia, a group known as OPEC+, comes ahead of a European Union embargo on Russian oil and would squeeze supplies in an already tight market, adding to inflation.

Given that production at some of the OPEC+ countries are below target levels, the actual cut would be smaller than the 2 million bpd reduction agreed to at the meeting.

Saudi Energy Minister Abdulaziz bin Salman said the real supply cut would be about 1 million to 1.1 million bpd and they were in response to rising interest rates in the West and a weakening global economy.

The administration of U.S. President Joe Biden has criticized the deal as being “shortsighted”. The White House said President Joe Biden would continue to assess whether to release further strategic oil stocks to lower prices.

The White House said it would consult with Congress on additional paths to reduce OPEC and its allies’ control over energy prices in an apparent reference to legislation that could expose members of the group to antitrust lawsuits.

“The final market impact would depend on the duration of the agreement, as OPEC+ decided to extend its Declaration of Cooperation until the end of 2023,” Citi analysts said in a note, adding that the supply cuts will keep global inventories low for longer and tighten markets in 2023.

More than half of the 1 million bpd supply cut is expected to come from world’s top exporter Saudi Arabia, analysts at RBC Capital said.

Separately on Wednesday, Russian Deputy Prime Minister Alexander Novak said Russia may cut oil output in an attempt to offset the effects of price caps imposed by the West over Moscow’s actions in Ukraine.

A draw in U.S. oil stockpiles last week also supported prices. Crude inventories dropped by 1.4 million barrels in the week ended Sept. 30 to 429.2 million barrels, the Energy Information Administration said.