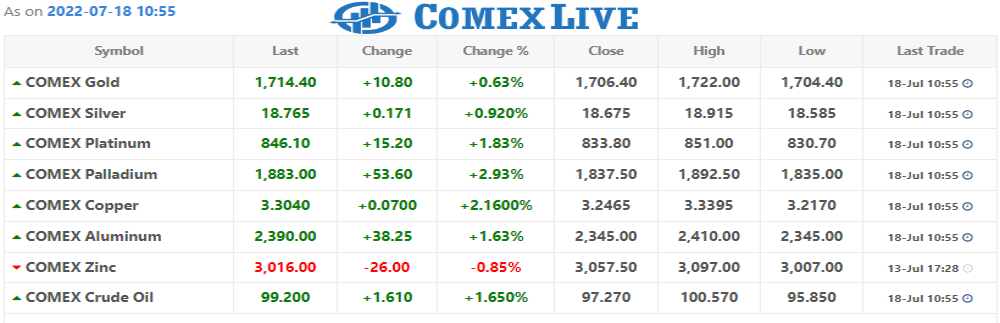

Oil prices extended gains on Monday, propped up by a weaker dollar and tight supplies that offset concerns about recession and the prospect of widespread Covid-19 lockdowns in China again reducing fuel demand.

Brent crude futures for September settlement rose $2.20, or 2.2%, to $103.36 a barrel, having advanced by 2.1% on Friday.

U.S. West Texas Intermediate (WTI) crude futures for August delivery gained $1.91, or 1.9%, to $99.50 after rising by 1.9% in the previous session.

The U.S. dollar retreated from multiyear highs on Monday, supporting prices of commodities ranging from gold to oil. A weaker dollar makes dollar-denominated commodities more affordable for holders of other currencies.

Both Brent and WTI last week registered their biggest weekly declines for about a month on fears of a recession that would hit oil demand. Mass Covid-testing exercises continue in parts of China this week, raising concerns over oil demand from the world’s second-largest oil consumer.

However, oil supplies remain tight. As expected, U.S. President Joe Biden’s trip to Saudi Arabia failed to yield any pledge from the top OPEC producer to boost oil supply.

Biden wants Gulf oil producers to step up output to help to lower oil prices and drive down inflation.

Global markets are focused this week on the resumption of Russian gas flows to Europe via the Nord Stream 1 pipeline, which is scheduled to end maintenance on July 21. Governments, markets and companies fear the shutdown could be extended because of the war in Ukraine.

“Brent crude will find support at the end of the week if Russia does not turn the gas back on to Germany after Nord Stream 1 maintenance,” said OANDA senior analyst Jeffrey Halley.

Loss of that gas to Germany, the world’s fourth-largest economy, would hit it hard and heighten the risk of recession.