Oil hit a multi-year high on Wednesday above $83 a barrel, supported by OPEC+’s refusal to ramp up production more rapidly against a backdrop of concern about tight energy supply globally. Later in the session, however, crude eased from its highs.

The market later unwound those gains due to an American Petroleum Institute (API) report showing rising crude inventories in the United States and, analysts said, technical indicators suggesting oil has rallied too fast.

On Monday, the Organization of the Petroleum Exporting Countries and allies, known as OPEC+, chose to stay with a plan to increase output gradually and not boost it further as the U.S. and other consumer nations have been urging.

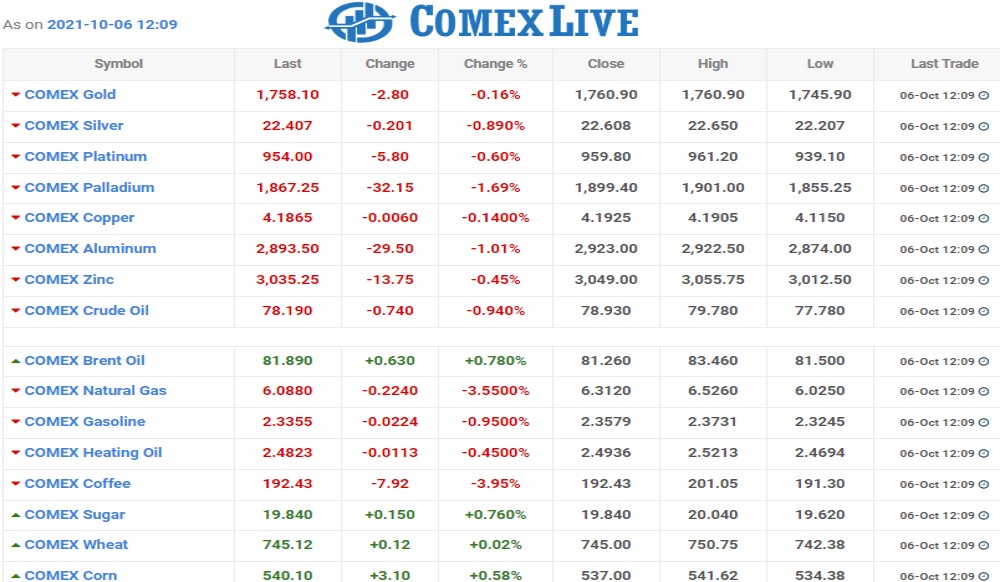

Brent crude rose as high as $83.47, the highest since October 2018, but was last down 38 cents at $82.16. U.S. crude climbed to $79.78, the highest since November 2014, but then retreated 35 cents to $78.58 per barrel.

“An energy crisis is unfolding with winter in the northern hemisphere still to begin, and sets the stage for even higher oil prices,” said Stephen Brennock of oil broker PVM.

The price of Brent has surged more than 50% this year, adding to inflationary pressure that could slow recovery from the COVID-19 pandemic. Natural gas has surged to a record peak in Europe and coal prices from major exporters have also hit all-time highs.

Jeffrey Halley, analyst at brokerage OANDA, said both crude contracts looked overbought based on a widely followed technical indicator, the relative strength index.

“That may signal some daily pullbacks this week but does not change the underlying bullish case for oil,” he said.

Some downward pressure came from the API’s figures showing signs of slowing fuel demand.

The industry group said U.S. crude inventories rose by 951,000 barrels in the week to Oct. 1, website Oilprice.com reported, and gasoline and distillate fuel inventories also climbed.

Attention will focus later on official inventory numbers due at 1430 GMT from the Energy Information Administration